|

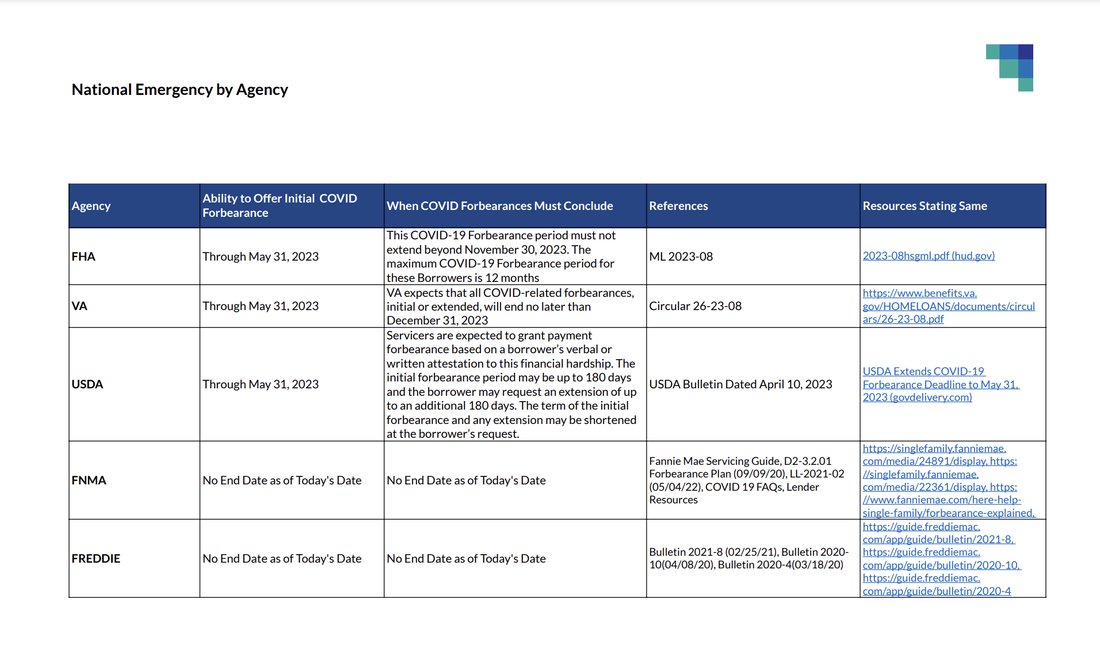

Introduced in the Senate on March 23, 2023, and referred to committee on March 29, 2023, Ohio Senate Bill 94, known in short form as the Bill that “regards the Treasurer of State, recorded instruments, liens, etc.,” sponsored by Senators Andrew O. Brenner (R) and Al Landis (R), seeks to amend numerous sections of the Ohio Revised Code related to recorded instruments, but also to enact section §5301.234, thereby codifying the doctrine of Equitable Subrogation. The legal doctrine of equitable subrogation permits one mortgagee to replace another mortgagee in lien priority and is typically claimed refinancing lenders who pay off the original mortgage and want to have the same priority as that lender. The doctrine seeks to prevent unjust enrichment and promote equity. Introduced in the Senate on January 23, 2023, and referred to committee on February 8, 2023, Ohio Senate Bill 25, known in short form as the Bill that “regards real property foreclosures,” sponsored by Senator Bob D. Hackett (R), seeks to alter the procedures for foreclosure sales. Chapter 2329 of the Ohio Revised Code currently governs execution upon judgments, including sales of real property resulting from foreclosure actions. SB25 proposes four significant changes to the foreclosure sale process that could result in a reduction in the length of time and cost of the foreclosure sale process: The United States Senate passed a resolution to end the National Emergency for COVID-19 on March 29, 2023, and the President signed it on Monday, April 10, ending the emergency earlier than May 11, 2023 as previously announced. Now that the National Emergency has ended, it is important to understand the implications for servicing, default, and loss mitigation. Below outlines the significance behind the ending of the National Emergency. This post includes Agency-specific updates covering:

Additional Loss Mitigation Resources

“The Delaware County Common Pleas Court General Division is now piloting a mediation program for civil cases. Any civil case may be referred to mediation based on a party’s motion and the approval of the court. The assigned judge may also refer any civil case for mediation. Parties may suggest a mediator from the approved mediator list, but the court will make the final selection and appointment of the mediator. The court will pay the approved mediator for the actual time spent in the matter, up to 8 hours of mediation time. In the event the mediator or the parties would like to request that the court pay for additional mediation time, they may file a motion with the court prior to incurring those expenses. This program does not prevent parties from utilizing a private mediator at their own expense. In order for the mediation cost to be covered under this pilot program, the parties must file a motion, receive approval from the court, and utilize a mediator from the court-approved mediator list.” Arkansas Legislature Amends Statutory Foreclosure Act in Response to Davis v. PennyMac Decision6/4/2021

Last year we alerted our clients and partners to the Arkansas Supreme Court ruling in Davis v. PennyMac Loan Services, LLC, 2020 Ark. 180 (May 7, 2020), wherein the Court held the sale notices used by some Arkansas law firms was too vague to satisfy the requirements of the Arkansas Statutory Foreclosure Act. To initiate a statutory foreclosure, the Statutory Foreclosure Act requires the recording of a Notice of Default and Intention to Sell (“Notice”) that states “the default for which the foreclosure is made.” Ark. Code Ann. § 18-50-104(b). The notice at issue in Davis stated that “a default has been made with respect to a provision in the mortgage.” The Court found that such boilerplate language was not a specific enough description of the default to satisfy the Statutory Foreclosure Act. Fortunately, PLG’s Arkansas foreclosures were not affected by the decision since its Notice contained the language required by the Statutory Foreclosure Act. The Court’s decision, however, created a realm of uncertainty related to statutory foreclosures completed by firms using the faulty notice. The status of all such REO properties became a topic of much concern, and the industry sought to resolve these issues through the passage of legislation amending the Statutory Foreclosure Act during the 2021 Regular Session of the Arkansas General Assembly. Thus, Act 1108 emerged, which will most likely become effective on July 30, 2021, although this date could change due to peculiarities in Arkansas law. Ohio's New Statute of Limitations on Breach of Written Contracts Goes Into Effect June 16, 20215/4/2021

Senate Bill 13 was signed into law on March, 16, 2021, and effectively shortens Ohio’s statute of limitations for filing lawsuits based on breach of contract. While R.C. 2305.06 originally set forth a lengthy 15-year statute of limitations on enforcement of a contract, the statute was amended in 2012 to reduce the limitation to eight years. The 2021 amendment to Revised Code 2305.07 now further reduces the statute of limitations for breaches of written contracts from eight years to six and reduces the statute of limitations for breaches of oral contracts from six years to four years. The new law goes into effect on June 16, 2021. |

|

|

Padgett Law Group and Padgett Law Group EP are D/B/As of Timothy D. Padgett, P.A. Timothy D. Padgett, P.A.'s practice areas include creditors' rights, estate planning and probate, real estate transactions and litigation. Not all practices or services are available in all states in which Timothy D. Padgett, P.A. practices.

PRIVACY STATEMENT | WEBSITE DESIGN BY SQFT.MANAGEMENT

|